A number of measures have been put in place to support Australians and the economy in response to the Coronavirus.

Our friends at MLC have put together some information to summarise the key measures and to assist you in understanding the help that could be available to you

When will the announced benefits become available?

All of the measures recently announced up to 22 March 2020 have now been legislated. While some benefits are available to be accessed immediately, others will commence in the coming weeks and months.

Outlined below is a summary of some of the key measures and important key dates.

Superannuation

Access to super savings

Access to superannuation savings has been broadened where you’re in financial distress because of the Coronavirus and meet certain eligibility conditions. If eligible, you’re able to access up to $10,000 before 30 June 2020 and an additional $10,000 from 1 July (available until approximately September).

To be eligible, you must meet one of the following conditions at the date you apply:

- you’re unemployed

- you’re eligible to receive Jobseeker Payment, Youth Allowance (jobseekers), Parenting Payment, Special Benefit or Farm Household Allowance

- on or after 1 January 2020, you were made redundant, your hours of work reduced by at least 20%, or if you’re a sole trader, your business was suspended or your turnover reduced by at least 20%.

You’ll also be able to make a withdrawal where you’re an employee of your own company or family trust and your working hours have decreased by at least 20%.

How to apply

Applications will be through MyGov to the Australian Taxation Office (ATO) and it is expected that claims can be made from mid-April.

You’ll need to make a declaration that you meet one of the above eligibility requirements. You’re also able to nominate how much you’d like (up to the $10,000 limit) and if you have multiple funds, you can also nominate more than one fund from which to draw this amount (up to a maximum of $10,000 in total).

Once the ATO confirms you’re eligible, it will issue you and your super fund with a determination and the payment will be made to you. If you have a self-managed super fund, arrangements will differ and the ATO is yet to provide those details.

Payments are tax-free and amounts received will not impact Centrelink or DVA entitlements.

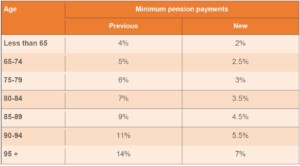

Income stream drawdown rates

There is a temporary reduction in the minimum annual amount that you’re required to withdraw from your super income stream. The reduction in the minimum drawdown rates applies for the duration of the 2019/20 financial year and for the 2020/21 financial year. The minimum drawdowns for account based pensions reduces as follows:

Business investment

Small business loans – relief package

Australian banks will provide support to eligible small businesses by deferring loan payments for up to six months, where assistance is required as a result of COVID-19. The intention is for banks to implement this as soon as possible. If you haven’t yet been contacted by your bank you should phone them to discuss your options.

Coronavirus Guarantee Scheme

The Coronavirus Guarantee Scheme will provide a Government guarantee of 50% of the value of new loans issued by eligible lenders to small and medium sized businesses. The intention of this measure is to increase access to loans by businesses impacted by the Coronavirus.

Additional lump sum payments to employers

Small and medium sized businesses and not-for-profit organisations (with turnover of less than $50m) that employ people will receive payments of between $20,000 and $100,000 to assist with operating expenses.

The amount will be made available in two instalments.

The amount of payment depends on whether your business is required to withhold tax on salary and wages for employees. If you don’t have employees, you won’t be eligible for these payments.

How much will I receive?

Where you’re required to withhold tax on salary and wages for employees, you’ll be entitled to an initial amount equal to 100% of the amount of tax withheld (up to a maximum of $50,000). Where you don’t actually withhold any tax, because for example, your employees earn amounts below the tax free threshold, you will still qualify for the minimum payment of $10,000. The second payment will be the same amount as the first payment, without any recalculation.

When will I receive the payments?

The payments will be tax free and received as a credit on the business’ activity statements by the ATO from 28 April 2020. The timing of the credit will vary depending on the required frequency of lodgement of activity statements (eg monthly or quarterly). All eligible businesses will receive a first payment of at least $10,000. Where this puts your business is a refund position, these amounts will be paid to you by the ATO within 14 days.

Instant asset write-off

From 12 March 2020, the instant write-off threshold will increase from $30,000 to $150,000. It has also been broadened and will be available to businesses with an annual turnover of up to $500 million for the current financial year (an increase from $50 million). This applies to new or second-hand assets used or installed ready for use by 30 June 2020. The increased write-off threshold will apply on a per asset basis until 30 June 2020.

Accelerated depreciation

Accelerated depreciation of 50% will apply to eligible assets until 30 June 2021. Eligible assets are those acquired after the announcement and are used or installed ready for use by 30 June 2020. However, it does not apply to second-hand assets, building or other capital works deductible under separate tax provisions. This concession will be available to business with aggregated turnover of less than $500 million.

Employers with apprentices and trainees

If you’re an eligible employer who employs apprentices or trainees, you can apply for a subsidy of 50% of the employee’s wage. This applies for the period of 1 January – 30 September 2020. The maximum payment is $21,000 per apprentice or trainee.

If you’re unable to retain an apprentice, the subsidy will be available to the new employer.

To be classified as an eligible employer, you must have less than 20 full-time employees. The apprentice or trainee must be in employment with a small business as at 1 March 2020. Other employers, regardless of size, and Group Training Organisations that re-engage eligible out-of-trade apprentices or trainees are also eligible for the subsidy.

Eligible employers can register for the subsidy from early April 2020 and final claims for payments lodged by 31 December 2020.

Social security

$750 cash payments

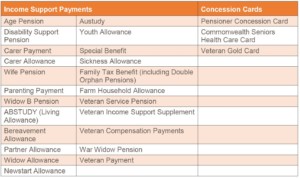

Two payments of $750 each will be paid to eligible income support recipients and concession card holders. The first tax-free payment is expected to be automatically paid to eligible recipients from 31 March 2020. The second payment will be available to those who aren’t eligible for the Coronavirus supplement (see below) and will be automatically paid from 13 July 2020. Eligibility for payment one To be eligible, you must be residing in Australia and have been eligible for one of the income support payments, or a holder of one of the concession cards listed in the table below on a day between 12 March and 13 April 2020. If you had applied for an eligible payment and are subsequently granted the payment, you will also be eligible for the one-off payment. These individuals will also be entitled to a second payment of $750 unless eligible for the Coronavirus supplement (see below).

Coronavirus Supplement

The Coronavirus supplement of $550 per fortnight will be paid to new and existing recipients of:

- JobSeeker Payment

- Youth Allowance (Jobseeker)

- Parenting Payment

- ABSTUDY

- Austudy

- Farm Household Allowance, and

- Special Benefit.

The supplement will be paid over the next six months and will be paid automatically with your ordinary fortnightly entitlement. It will be paid from 27 April.

Existing social security recipients -change in circumstances

If you’re already receiving a particular benefit or payment and your circumstances change due to COVID-19, your benefit may remain unchanged. However, a change in circumstances that is not a result of COVID-19 will be assessed under the ordinary rules, and may impact your entitlement. All changes should be reported to Centrelink or DVA within 14 days.

- Recipients of Carer Payment who are impacted will not have their benefits changed.

- Child Care Subsidy: if your child cannot attend childcare as a result of COVID-19, but you’re still charged a fee from your childcare provider, you may still receive the subsidy for up to 42 days of absence. This applies also to non-COVID-19 related absences. If your activity hours change, you don’t need to update your activity tests where it is due to a requirement to self isolate, or if you’re on leave.

- Newstart or Jobseeker: Recipients with mutual obligations (for example Newstart or Jobseeker recipients who usually need to be actively looking for work, volunteering, or doing some paid work) will be provided flexible options to ensure your safety. This may apply where you’re unable to satisfy these requirements because you’re self-isolating, or you’re a primary carer, caring for a child whose school has closed, or a disabled adult whose day service closes. You may receive an exemption from this requirement without a need for medical evidence.

- Youth Allowance (student): Activity requirements for study will be amended. This means that if you’re a student and you’re unable to attend studies due to the virus, you may be exempt from meeting this requirement.

- Students and trainees: If you’re self isolating at home or your education provider closes or reduces your study load, your payment won’t change. You must remain enrolled in study and have a plan to return and must tell Centrelink if this doesn’t apply to you.

Applying for a new benefit – impacted by COVID-19

Depending on your circumstances, you may be eligible to apply for a number of payments. You may have been stood down, made redundant, or have had your hours significantly reduced. It’s also possible that you’ve needed to stop working to care for someone.

Also, if you’re unable to work, are in isolation or hospital, or you need to care for children as a result of COVID-19, you may also be eligible to apply for a payment for a period of time.

Ordinarily, most benefits and concession cards have either an income test, and assets test, or both, to determine your eligibility. However, if you apply for a social security benefit or concession card and your claim is related to COVID-19, some of the ordinary eligibility rules may be waived for approximately six months. Also, if you’re an employee, and you are diagnosed with COVID-19 or are in isolation, you may be eligible for an income support payment if you are not also accessing employer leave entitlements, or income protection policy benefits.

If you’re a sole trader or you’re self-employed you may also be eligible for a payment if your business has been suspended or turnover has reduced significantly.

New category of Crisis Payment

Individuals claiming an income support payment may be eligible for a Crisis Payment under a proposed new category, if they are required to self-isolate at home due to the Coronavirus.

At the time of claiming the Crisis Payment, a person must:

- have made a claim and qualify for an income support payment, and

- satisfy requirements of any legislative instruments made by the Minister, including the need to self-isolate.

The one-off Crisis Payment is tax-free and is equal to one week your income support payment (basic rate).

Waiting periods and assets testing

The ordinary one week waiting period that applies to some payments is waived when claiming because you’re impacted by COVID-19. The Liquid Assets Waiting Period (LAWP) is also waived if you’re entitled to the Coronavirus Supplement.

If you’ve already applied for a payment and are currently serving a LAWP, you won’t need to serve the remainder of the waiting period. This also applies if you’ve applied for a payment which is eligible for the Coronavirus Supplement.

The Income Maintenance Period and Compensation Preclusion Periods continue to apply. This means that if you’ve received a redundancy payment or a lump sum amount of unused leave entitlements, you may not be eligible for a payment straight away.

The assets test is not applied when determining your entitlement to JobSeeker Payment, Youth Allowance (Jobseeker) and Parenting Payment for six months. The income test continues to apply and may reduce the amount of the payment you’re eligible for. If you’re a member of a couple, your partner’s income is taken into account when determining your eligibility.

To access these measures, recipients of JobSeeker Allowance and Youth Allowance (Jobseeker) cannot be receiving employer benefits (such as sick leave or annual leave payments) or income protection payments at the same time.

Reduction in deeming rates

A further reduction in deeming rates was announced on 22 March. The deeming rates will reduce as follows:

The deeming thresholds are unchanged at $51,800 (single) and $86,200 (couple) which are generally indexed on 1 July each year. The rates will take effect from 1 May 2020, and any additional entitlement will be paid from that date.

Other measures

Additional measures announced include:

- Support for regions and communities impacted by the virus with reliance on tourism, agriculture and education

- Administrative relief provided by the ATO for certain tax obligations, such as lodging tax returns and activity statements, which will be assessed based on individual circumstances, and

- Comprehensive health package of $2.4 billion.

You may wish to contact the ATOs Emergency Support Infoline on 1800 806 218 or email COVID-19Taxissues@ato.gov.au.

Important information

This document has been prepared by GWM Adviser Services Limited (ABN 96 002 071 749, AFSL 230692) (GWMAS), part of the National Australia Bank group of companies. Any advice provided is of a general nature only. It does not take into account your objectives, financial situation or needs. Please seek personal advice before making a decision about a financial product. Information in this document is current as at 25 March 2020. While care has been taken in its preparation, no liability is accepted by GWMAS or its related entities, agents or employees for any loss arising from reliance on this document. Any opinions expressed constitute our views as at 25 March 2020. Case studies are for illustration purposes only. Any tax information provided is a guide only. It is not a substitute for specialised tax advice. GWM Adviser Services Limited (ABN 96 002 071 749, AFSL 230692) (‘GWMAS’). A member of the National Australia Bank Limited (‘NAB’) group of companies. NAB does not guarantee or otherwise accept any liability in respect of GWMAS or these services.